UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K/A

(Amendment No. 1)

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of Earliest Event Reported): April 2, 2026

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation) | (Commission File Number) | (I.R.S. Employer Identification No.) | ||||||||||||

(Address of principal executive offices)

(Zip Code)

Registrant’s telephone number, including area code: (734 ) 887-3903

Not Applicable

Former name or former address, if changed since last report

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 or Rule 12b-2 of the Securities Exchange Act of 1934.

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Explanatory Note

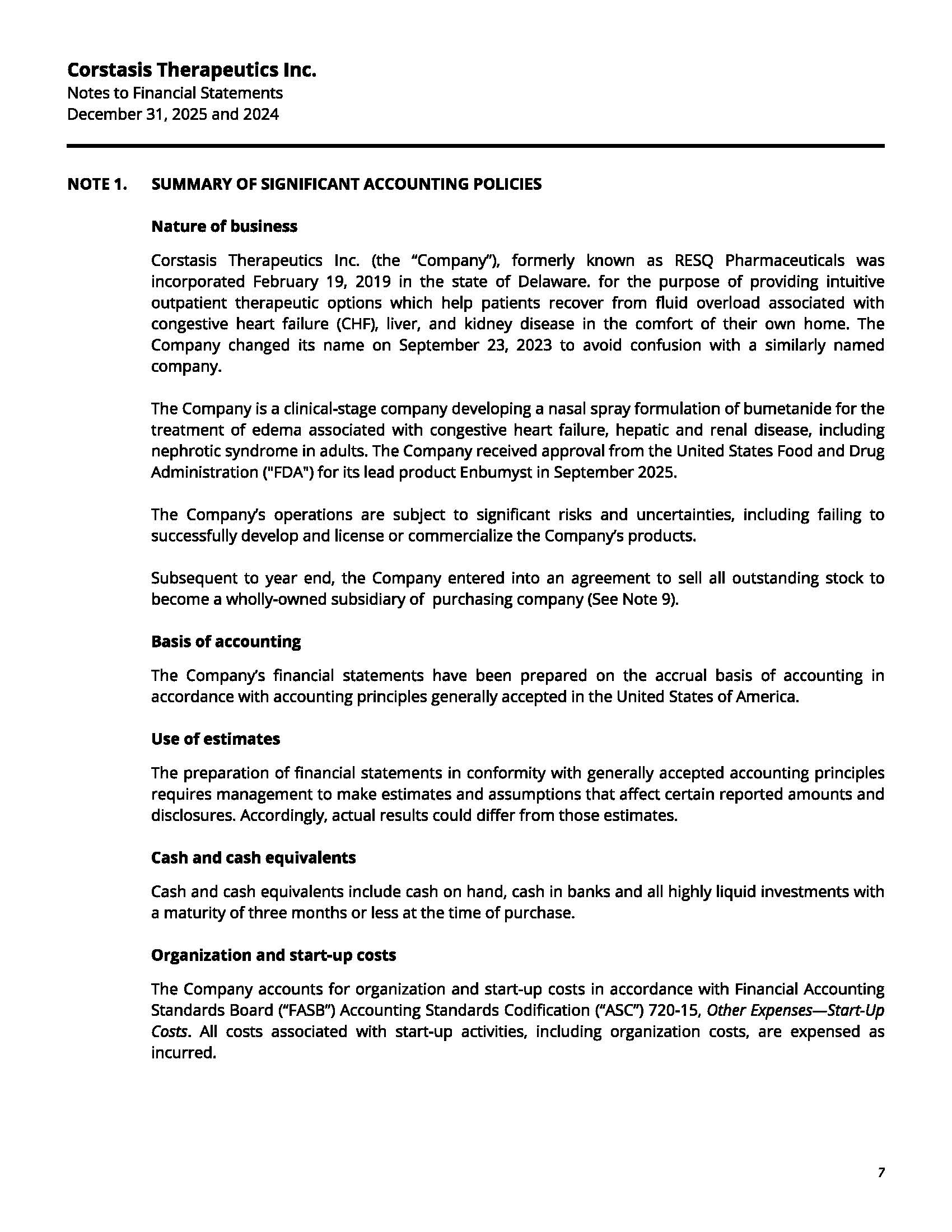

On April 2, 2026, Esperion Therapeutics, Inc. (the “Company”) filed a Current Report on Form 8-K (the “Original Report”) to report, among other things, the completion of its previously announced acquisition (the “Merger”) of all of the issued and outstanding stock of Corstasis Therapeutics Inc., a Delaware corporation (“Corstasis”), pursuant to an Agreement and Plan of Merger, dated as of March 2, 2026, by and among the Company, Corstasis, Cirrus Transaction Subsidiary, Inc., a Delaware corporation and wholly owned subsidiary of the Company, and certain other parties described therein (the “Merger Agreement”).

The Company is filing this Current Report on Form 8-K/A (the “Amendment”) solely to amend Item 9.01 of the Original Report to present the required financial statements and pro forma financial information not later than 71 calendar days from the date on which the Original Report was required to be filed, as permitted under Items 9.01(a)(3) and 9.01(b)(2). Except for the filing of such financial statements and pro forma financial information, this Amendment does not otherwise modify or update the Original Report, and this Amendment should be read in conjunction with the Original Report.

Item 9.01. Financial Statements and Exhibits.

(a) Financial Statements of Business Acquired

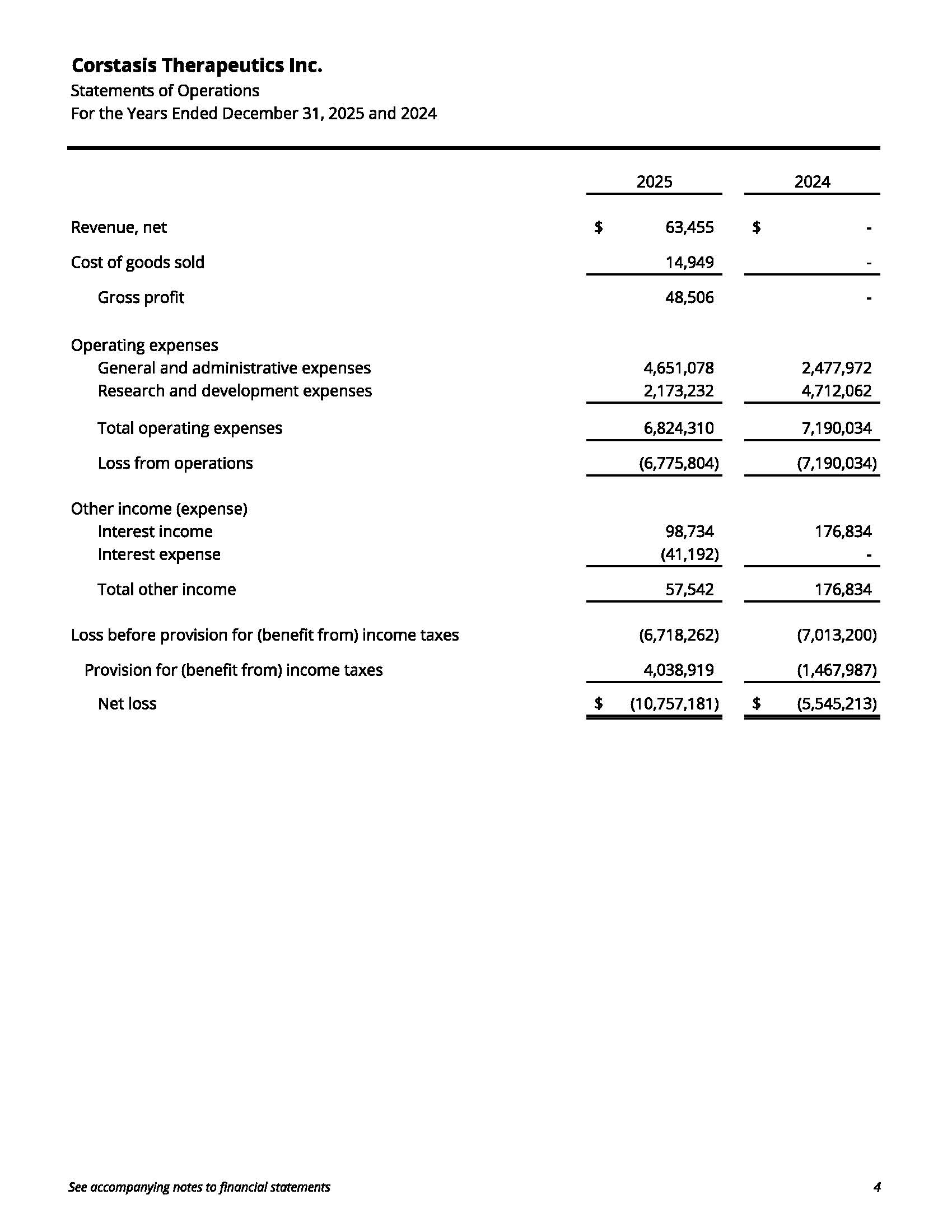

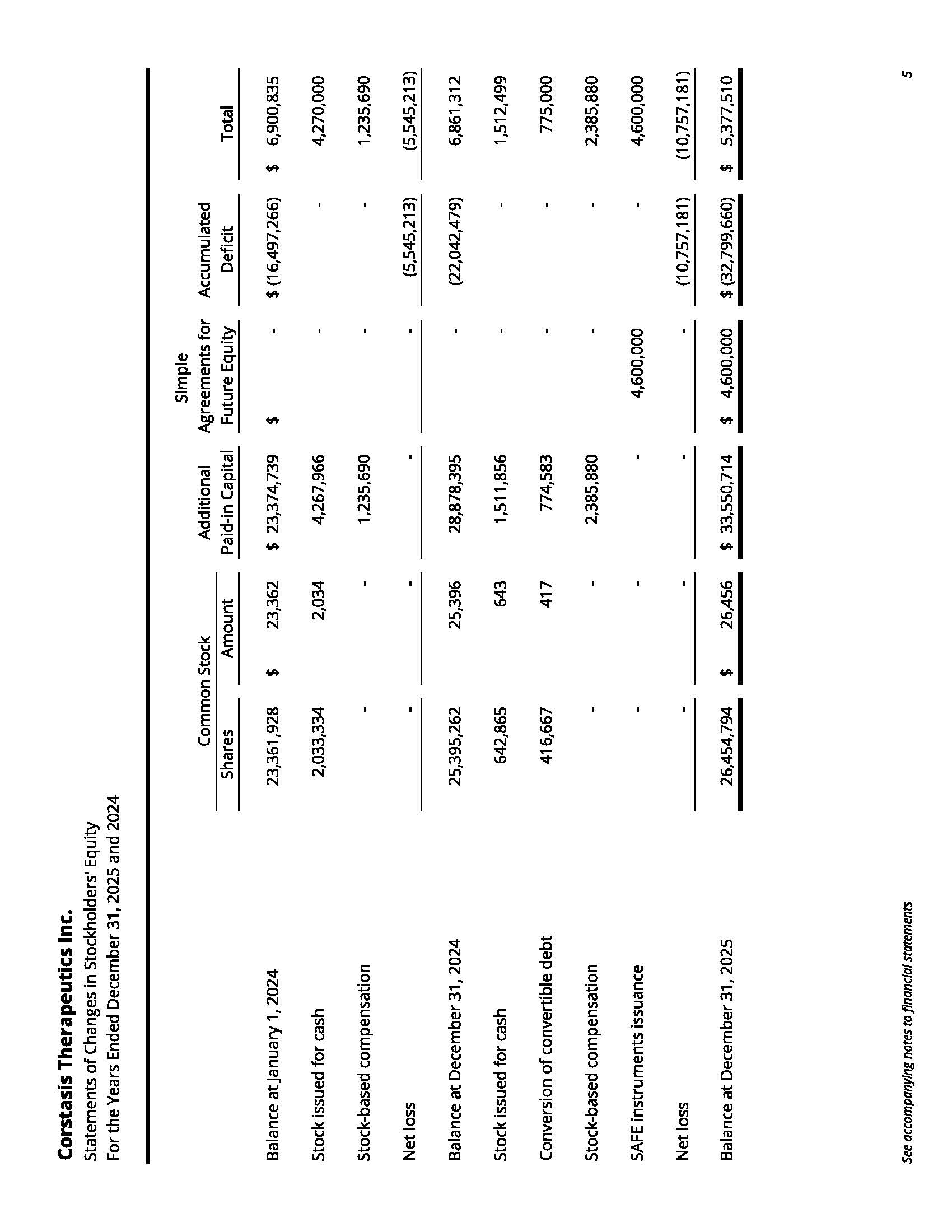

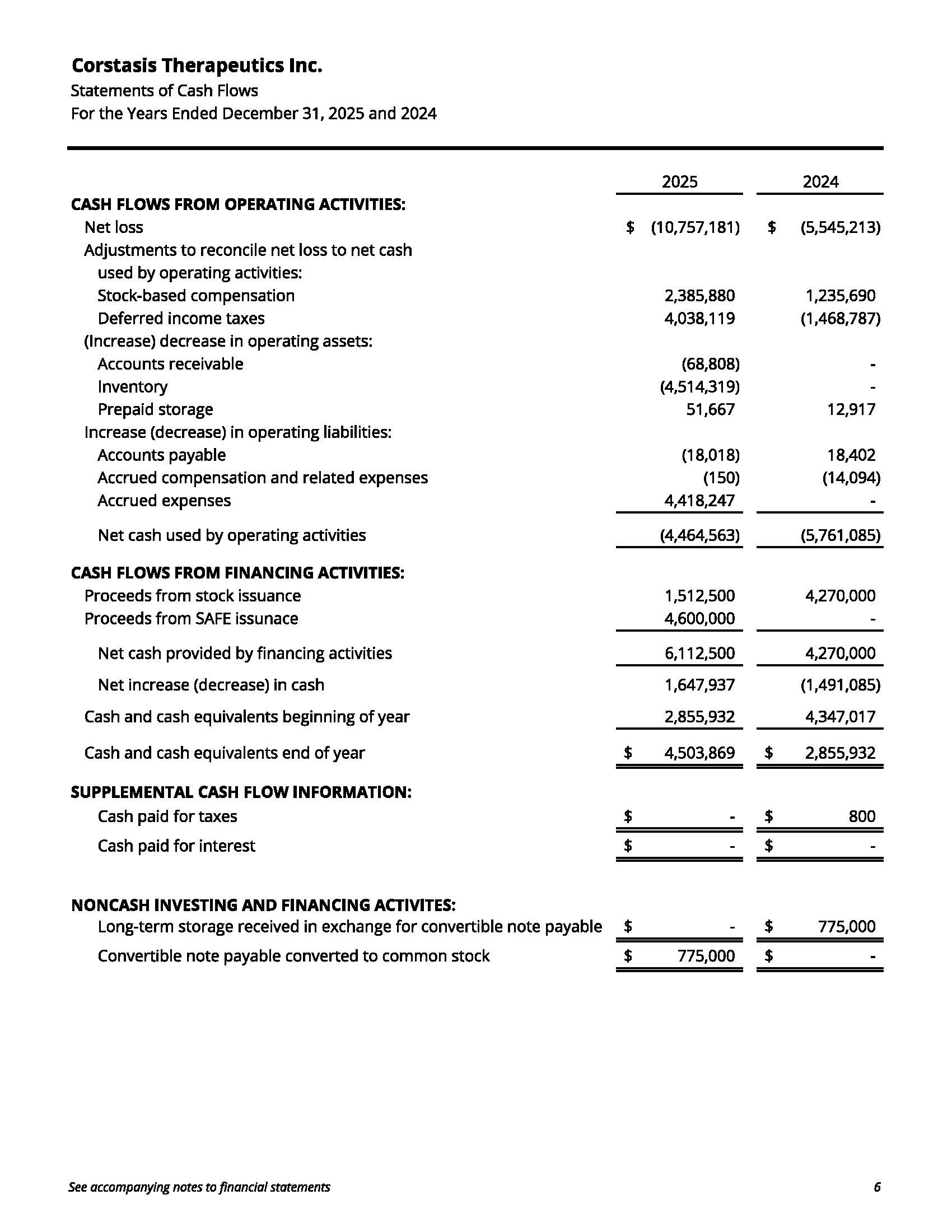

The audited consolidated financial statements of Corstasis as of and for the years ended December 31, 2025 and 2024, and the related notes thereto are filed as Exhibit 99.1 hereto and are incorporated herein by reference.

(b) Pro Forma Financial Information

The unaudited pro forma condensed combined balance sheet of the Company as of December 31, 2025, and the unaudited pro forma condensed combined statements of earnings of the Company for the fiscal year ended December 31, 2025, giving pro forma effect to the acquisition of Corstasis are filed as Exhibit 99.2 hereto and are incorporated herein by reference.

(d) Exhibits.

| Exhibit No. | Description | |||||||

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL Document). | |||||||

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| Date: June 18, 2026 | Esperion Therapeutics, Inc. | |||||||

| By: | /s/ Sheldon L. Koenig | |||||||

| Sheldon L. Koenig | ||||||||

| President and Chief Executive Officer | ||||||||

Exhibit 23.1

Consent of Independent Auditors

We consent to the incorporation by reference in the following Registration Statements:

•Registration Statement (Form S-3 No. 333-286631) of Esperion Therapeutics, Inc.

•Registration Statement (Form S-8 No. 333-289575) pertaining to the 2022 Stock Option and Incentive Plan, as amended, of Esperion Therapeutics, Inc.

•Registration Statement (Form S-8 No. 333-281486) pertaining to the 2022 Stock Option and Incentive Plan, as amended, of Esperion Therapeutics, Inc. and the 2020 Employee Stock Purchase Plan, as amended, of Esperion Therapeutics, Inc.

•Registration Statement (Form S-8 No. 333-274183) pertaining to the Amended 2017 Inducement Equity Plan, as amended, of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333-273555) pertaining to the 2022 Stock Option and Incentive Plan, as amended, of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333-265247) pertaining to the 2022 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333-262881) pertaining to the Amended and Restated 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333-253414) pertaining to the Amended and Restated 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333-243757) pertaining to the 2020 Employee Stock Purchase Plan, as amended, of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333-236712) pertaining to the Amended and Restated 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc. and the 2017 Inducement Equity Plan, as amended, of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333‑228994) pertaining to the Amended and Restated 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333‑223105) pertaining to the Amended and Restated 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333‑218084) pertaining to the 2017 Inducement Equity Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333‑216169) pertaining to the Amended and Restated 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333‑208702) pertaining to the Amended and Restated 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333‑206180) pertaining to the Amended and Restated 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333‑201378) pertaining to the 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

•Registration Statement (Form S‑8 No. 333‑194536) pertaining to the 2013 Stock Option and Incentive Plan of Esperion Therapeutics, Inc.

of our report dated June 5, 2026, with respect to the financial statements of Corstasis Therapeutics Inc. included in this Current Report on Form 8-K/A of Esperion Therapeutics, Inc. dated June 18, 2026.

/s/ Redwitz, Inc.

Irvine, California

June 18, 2026

Exhibit 99.1

Exhibit 99.2

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL STATEMENTS

On April 2, 2026 (the "Closing Date"), Esperion Therapeutics, Inc. (the "Company") completed the acquisition of Corstasis Therapeutics, Inc. ("Corstasis") pursuant to an Agreement and Plan of Merger (the "Merger Agreement"), by and among the Company, Cirrus Transaction Subsidiary, Inc., a Delaware corporation and wholly-owned subsidiary of the Company ("Merger Sub"), and Corstasis, pursuant to which Merger Sub merged with and into Corstasis, with Corstasis surviving the merger as a wholly-owned subsidiary of the Company (the "Acquisition"). The following unaudited pro forma condensed combined financial statements and related notes have been prepared to give effect to the Acquisition and the related Financing Transactions defined and described below.

The Company has preliminarily concluded that the Acquisition will be treated as an asset acquisition under Accounting Standards Codification ("ASC") 805, Business Combinations (“ASC 805”), as the set of assets and activities acquired does not meet the definition of a business under ASC 805-10-55, including as amended by ASU 2017-01. Accordingly, the Acquisition has been accounted for using the cost accumulation and allocation model in accordance with ASC 805-50, Business Combinations — Related Issues, whereby the total cost of the Acquisition, including transaction costs, is allocated to the identifiable assets acquired and liabilities assumed based on their relative fair values at the Closing Date, with no goodwill recognized.

The unaudited pro forma condensed combined financial statements have been prepared in accordance with Article 11 of Regulation S-X, Pro Forma Financial Information, as amended (“Article 11”). Article 11 provides simplified requirements to depict the accounting for the transaction (“Transaction Accounting Adjustments”) and the option to present the reasonably estimable synergies and other transaction effects that have occurred or are reasonably expected to occur (“Management’s Adjustments”). The Company has elected not to present Management’s Adjustments in the unaudited pro forma condensed combined financial statements.

The unaudited pro forma condensed combined balance sheet as of December 31, 2025 gives effect to the Acquisition as if it had occurred on December 31, 2025. The unaudited pro forma condensed combined statement of operations for the year ended December 31, 2025 gives effect to the Acquisition as if it had occurred on January 1, 2025, the beginning of the earliest period presented.

In connection with the Acquisition, the Company obtained $75.0 million in financing through two concurrent transactions (collectively, the “Financing Transactions”). The aggregate proceeds of $75.0 million were used to fund the Acquisition and related transaction costs. The Financing Transactions are described below.

•Pursuant to the First Amendment to the Credit Agreement, dated as of April 2, 2026 (the "First Amendment"), among the Company, as borrower, certain subsidiaries of the Company, as guarantors, the lenders party thereto, and GLAS USA LLC and GLAS Americas LLC, as administrative agent and collateral agent, the Company borrowed an additional $25.0 million in term loans (the "First Amendment Term Loan") under its existing Credit Agreement dated December 13, 2024. The First Amendment Term Loan bears interest at a rate of 9.75% per annum on the same terms as the outstanding term loans under the Credit Agreement and are subject to prepayment premiums on a sliding scale.

•Pursuant to the Royalty Purchase Agreement, dated as of April 2, 2026 (the "Royalty Purchase Agreement"), between the Company, as seller, and Athyrium Opportunities IV Acquisition LP ("Athyrium"), as purchaser, the Company received proceeds of $50.0 million in exchange for the sale of 100% of the royalty payments and regulatory and commercial milestone payments payable to the Company by Otsuka Pharmaceutical Co., Ltd. under the License and Collaboration Agreement, dated as of April 17, 2020, as amended, with respect to net sales of licensed products in the Otsuka territory, in each case until Athyrium has received aggregate net payments of $100.0 million (the "Cap Amount"). For U.S. federal

income tax purposes, the Royalty Purchase Agreement is treated as a contingent payment debt instrument issued with original issue discount, and not as a sale of receivables.

The unaudited pro forma condensed combined financial statements are based on, and should be read in conjunction with:

•The Company's audited consolidated financial statements and related notes included in the Company's Annual Report on Form 10-K for the year ended December 31, 2025; and

•The historical financial statements of Corstasis for the year ended December 31, 2025 and accompanying notes filed as exhibits to this Form 8-K/A.

The Transaction Accounting Adjustments are preliminary and are based upon available information and certain assumptions, as described in the accompanying notes to the unaudited pro forma condensed combined financial statements, which the Company believes are reasonable under the circumstances.

The unaudited pro forma condensed combined financial statements are provided for illustrative purposes only and does not purport to represent what the actual financial position or results of operations of the Company would have been had the Acquisition occurred on the dates indicated, nor is it necessarily indicative of the Company's future financial position or results of operations. The unaudited pro forma condensed combined financial statements do not reflect the costs of any integration activities, or any synergies, operational efficiencies, or other costs or benefits that may result from the Acquisition.

UNAUDITED PRO FORMA CONDENSED COMBINED BALANCE SHEET

AS OF DECEMBER 31, 2025

(in thousands, except share data)

As of December 31, 2025 | As of December 31, 2025 | |||||||||||||||||||||||||

Esperion Therapeutics, Inc. (Historical) | Corstasis Therapeutics Inc. (Historical) | Transaction Accounting Adjustments | Note Ref | Financing Accounting Adjustments | Note Ref | Pro Forma Combined | ||||||||||||||||||||

Assets | ||||||||||||||||||||||||||

Current assets: | ||||||||||||||||||||||||||

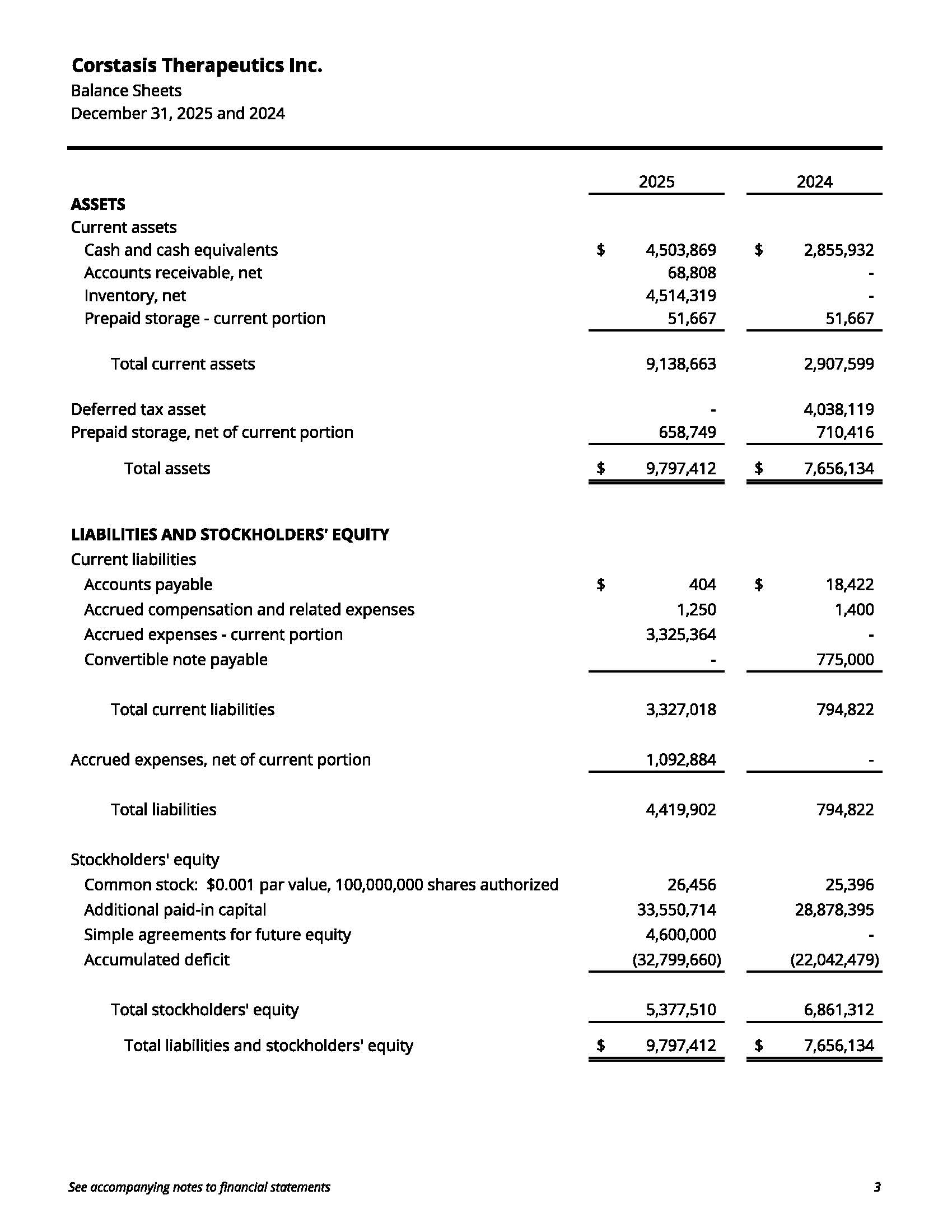

Cash and cash equivalents | $ | 167,852 | $ | 4,504 | $ | (83,389) | (A) | $ | 24,088 | (C) | $ | 161,743 | ||||||||||||||

48,688 | (D) | |||||||||||||||||||||||||

Accounts receivable, net | 140,190 | 69 | — | — | 140,259 | |||||||||||||||||||||

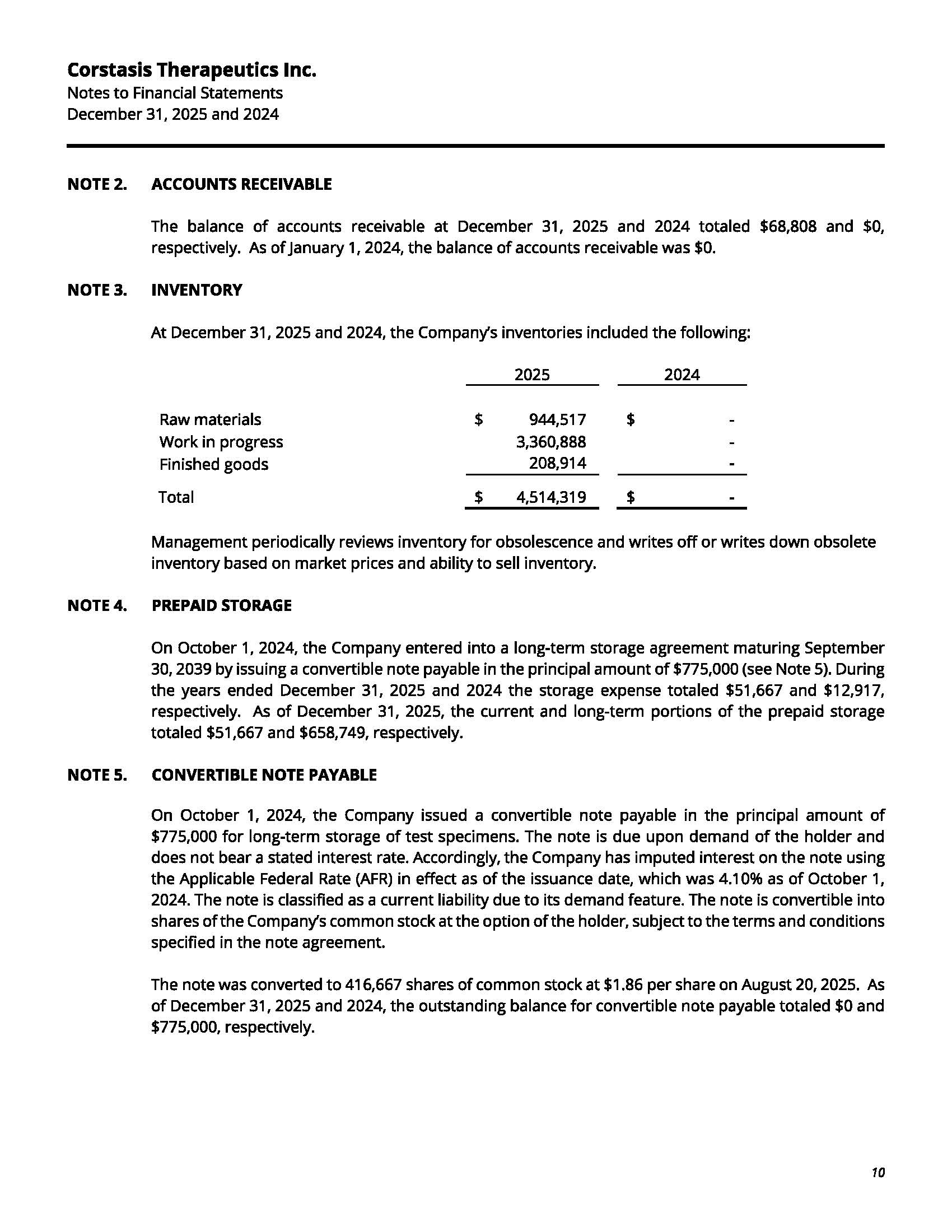

Inventories, net | 105,124 | 4,514 | 915 | (A) | — | 110,553 | ||||||||||||||||||||

Prepaid clinical development costs | 4,044 | — | — | — | 4,044 | |||||||||||||||||||||

Prepaid inventory costs | 40,864 | — | — | — | 40,864 | |||||||||||||||||||||

Other prepaid and current assets | 4,496 | 52 | — | — | 4,548 | |||||||||||||||||||||

Total current assets | 462,570 | 9,139 | (82,474) | 72,776 | 462,011 | |||||||||||||||||||||

Property and equipment, net | 338 | — | — | — | 338 | |||||||||||||||||||||

Right of use operating lease assets | 2,922 | — | — | — | 2,922 | |||||||||||||||||||||

Prepaid storage, net of current portion | — | 659 | — | — | 659 | |||||||||||||||||||||

Intangible assets | 56 | — | 77,097 | (A) | — | 77,153 | ||||||||||||||||||||

Total assets | $ | 465,886 | $ | 9,798 | $ | (5,377) | $ | 72,776 | $ | 543,083 | ||||||||||||||||

Liabilities and stockholders' deficit | ||||||||||||||||||||||||||

Current liabilities: | ||||||||||||||||||||||||||

Accounts payable | $ | 65,068 | $ | — | $ | — | $ | — | $ | 65,068 | ||||||||||||||||

Accrued clinical development costs | 4,115 | — | — | — | 4,115 | |||||||||||||||||||||

Accrued variable consideration | 88,203 | — | — | — | 88,203 | |||||||||||||||||||||

Other accrued liabilities | 19,249 | 3,327 | — | — | 22,576 | |||||||||||||||||||||

Royalty sale liability, current | 87,596 | — | — | 4,648 | (D) | 92,244 | ||||||||||||||||||||

Deferred revenue from collaborations | 34,477 | — | — | — | 34,477 | |||||||||||||||||||||

Operating lease liabilities | 2,102 | — | — | — | 2,102 | |||||||||||||||||||||

Total current liabilities | 300,810 | 3,327 | — | 4,648 | 308,785 | |||||||||||||||||||||

Convertible notes, net of issuance costs | 97,260 | — | — | — | 97,260 | |||||||||||||||||||||

Royalty sale liability, non-current | 208,170 | — | — | 44,040 | (D) | 252,210 | ||||||||||||||||||||

Long-term debt | 152,219 | — | — | 24,088 | (C) | 176,307 | ||||||||||||||||||||

Operating lease liabilities | 653 | — | — | — | 653 | |||||||||||||||||||||

Other long-term liabilities | 8,739 | 1,094 | — | — | 9,833 | |||||||||||||||||||||

Total liabilities | $ | 767,851 | $ | 4,421 | $ | — | $ | 72,776 | $ | 845,048 | ||||||||||||||||

Commitments and contingencies | ||||||||||||||||||||||||||

Stockholders’ deficit: | ||||||||||||||||||||||||||

Common stock, $0.001 par value | 245 | 26 | (26) | (B) | — | 245 | ||||||||||||||||||||

Additional paid-in capital | 1,376,499 | 38,151 | (38,151) | (B) | — | 1,376,499 | ||||||||||||||||||||

Treasury stock, at cost | (54,998) | — | — | — | (54,998) | |||||||||||||||||||||

Accumulated deficit | (1,623,711) | (32,800) | 32,800 | (B) | — | (1,623,711) | ||||||||||||||||||||

Total stockholders' deficit | (301,965) | 5,377 | (5,377) | — | (301,965) | |||||||||||||||||||||

Total liabilities and stockholders' deficit | $ | 465,886 | $ | 9,798 | $ | (5,377) | $ | 72,776 | $ | 543,083 | ||||||||||||||||

UNAUDITED PRO FORMA CONDENSED COMBINED STATEMENT OF OPERATIONS

YEAR ENDED DECEMBER 31, 2025

(in thousands, except share and per share data)

Twelve Months Ended December 31, 2025 | Twelve Months Ended December 31, 2025 | Twelve Months Ended December 31, 2025 | |||||||||||||||||||||||||||||||||

Esperion Therapeutics, Inc. (Historical) | Corstasis Therapeutics Inc. (Historical) | Transaction Accounting Adjustments | Note Ref | Financing Accounting Adjustments | Note Ref | Pro Forma Combined | |||||||||||||||||||||||||||||

Revenues: | |||||||||||||||||||||||||||||||||||

Product sales, net | $ | 159,569 | $ | 63 | $ | — | $ | — | $ | 159,632 | |||||||||||||||||||||||||

Collaboration revenue | 243,566 | — | — | — | 243,566 | ||||||||||||||||||||||||||||||

Total Revenues | 403,135 | 63 | — | — | 403,198 | ||||||||||||||||||||||||||||||

Operating expenses: | |||||||||||||||||||||||||||||||||||

Cost of goods sold | 129,224 | 15 | — | — | 129,239 | ||||||||||||||||||||||||||||||

Research and development | 47,852 | 2,173 | — | — | 50,025 | ||||||||||||||||||||||||||||||

Selling, general and administrative | 165,786 | 4,651 | 7,710 | (AA) | — | 178,147 | |||||||||||||||||||||||||||||

Total operating expenses | 342,862 | 6,839 | 7,710 | — | 357,411 | ||||||||||||||||||||||||||||||

Income (loss) from operations | 60,273 | (6,776) | (7,710) | — | 45,787 | ||||||||||||||||||||||||||||||

Interest expense | (84,604) | (41) | — | (9,953) | (BB), (DD) | (94,598) | |||||||||||||||||||||||||||||

Other income, net | 3,490 | 99 | — | — | 3,589 | ||||||||||||||||||||||||||||||

Loss before income taxes | (20,841) | (6,718) | (7,710) | (9,953) | (45,222) | ||||||||||||||||||||||||||||||

Provision for taxes on income | 1,841 | 4,039 | (4,039) | (CC) | — | 1,841 | |||||||||||||||||||||||||||||

Net loss | $ | (22,682) | $ | (10,757) | $ | (3,671) | $ | (9,953) | $ | (47,063) | |||||||||||||||||||||||||

Net loss per common share (basic and diluted) | $ | (0.11) | $ | (0.23) | (EE) | ||||||||||||||||||||||||||||||

Weighted-average shares outstanding (basic and diluted) | 207,865,080 | — | — | — | 207,865,080 | ||||||||||||||||||||||||||||||

1. Description of the Contemplated Transactions and Basis of Presentation

Acquisition of Corstasis Therapeutics, Inc. and Related Financing Transactions

On March 2, 2026, the Company entered into an Agreement and Plan of Merger with Corstasis and Merger Sub, which provided for Merger Sub to merge with and into Corstasis, with Corstasis surviving the merger as a wholly-owned subsidiary of the Company. The Acquisition closed on April 2, 2026. Consideration paid by the Company is detailed in Note 2. To fund the Acquisition, the Company obtained an aggregate of $75.0 million through Financing Transactions described above.

In determining the appropriate accounting treatment for the Acquisition, the Company first evaluated whether the acquired set of assets and activities meets the definition of a business under ASC 805. As an initial step, the Company applied the concentration screen under ASC 805-10-55-5A to determine whether substantially all of the fair value of the gross assets acquired is concentrated in a single identifiable asset or group of similar assets.

The Company concluded that substantially all of the fair value of the gross assets acquired from Corstasis is concentrated in Enbumyst, a single developed product intangible asset. As a result of the concentration screen, the acquired set is not considered a business, and the Company will account for the Acquisition as an asset acquisition in accordance with ASC 805-50, Business Combinations — Related Issues. Under the asset acquisition method of accounting, the total acquisition cost, including all direct transaction costs, is allocated to the identifiable assets acquired and liabilities assumed on a relative fair value basis, with no goodwill recognized. As Enbumyst has an alternative future use, evidenced by FDA approval on September 12, 2025, it will be capitalized and amortized over its estimated useful life.

Basis of Presentation

The unaudited pro forma condensed combined financial statements have been prepared in accordance with Article 11. The adjustments in the unaudited pro forma condensed combined financial statements have been identified and presented to provide relevant information necessary for an illustrative understanding of the Company upon consummation of the Acquisition and the related Financing Transactions in accordance with accounting principles generally accepted in the United States.

The assumptions and estimates underlying the unaudited Transaction Accounting Adjustments presented in the unaudited pro forma condensed combined financial statements are described in the accompanying notes. The unaudited pro forma condensed combined financial statements have been presented for illustrative purposes only and are not necessarily indicative of the operating results and financial position that would have been achieved had the Acquisition occurred on the dates indicated. Further, the unaudited pro forma condensed combined financial statements do not purport to project the future operating results or financial position of the Company following the consummation of the Acquisition. The unaudited Transaction Accounting Adjustments represent management’s estimates based on information available as of the date of the unaudited pro forma condensed combined financial statements and are subject to change as additional information becomes available and analyses are performed. For pro forma purposes, no income tax benefit has been recognized on any Transaction Accounting Adjustment, as the Company maintains a full valuation allowance against its net deferred tax assets. The Company and Corstasis had no historical relationship prior to the Acquisition. Accordingly, no Transaction Accounting Adjustments were required to eliminate activities between the companies.

2. Estimate of the Cost of the Asset Acquisition

The Company determined the total cost to acquire the assets of Corstasis based on the following components:

Consideration paid in the Acquisition consisted of:

•a cash payment of $77.5 million to Corstasis; and

•direct transaction costs of the Company of $5.9 million.

The Merger Agreement additionally provides for future contingent cash payments consisting of:

•a one-time regulatory milestone payment of $20.0 million upon the first FDA approval of a Follow-on Product for commercialization in the United States;

•tiered commercial milestone payments upon the achievement of specified cumulative Net Sales thresholds up to $160.0 million;

•earn-out payments equal to 15% of Net Sales of Earn-Out Products on a product-by-product and country-by-country basis during the applicable earn-out payment term, which commences on the date of the First Commercial Sale of each Earn-Out Product in each country and expires upon the latest of patent expiry, loss of regulatory exclusivity, or the tenth anniversary of the First Commercial Sale in such country, subject to reduction upon significant generic entry; and

•licensing revenue payments equal to 15% of consideration received from third-party licenses or sublicenses of the Product or any Follow-on Product in the Territory, and 30% or 20%, respectively, of ex-U.S. royalties received from third-party licensees on net sales of the Product or any Follow-on Product.

As the transaction was accounted for as an asset acquisition and the future contingent cash payments meet various exceptions under ASC 815, Derivatives and Hedging, and are not considered probable on the acquisition date under ASC 450, Contingencies, the contingent cash payments are not included in the initial cost of the Acquisition.

3. Transaction Accounting Adjustments

The following adjustments are reflected in the unaudited pro forma condensed combined balance sheet as of December 31, 2025:

A.Represents the capitalization of the total cost of the Acquisition and its allocation to the assets and liabilities on a relative fair value basis in accordance with the cost accumulation and allocation model under ASC 805-50. The following table summarizes the cost of the acquisition:

Amount | |||||

(in thousands) | |||||

Cash consideration to Seller | $ | 77,460 | |||

Buyer acquisition costs | 5,929 | ||||

Total cost of acquisition | $ | 83,389 | |||

The following table summarizes the preliminary allocation of the above purchase consideration based on the relative fair value of the assets acquired:

Amount | ||||||||

(in thousands) | ||||||||

Assets purchased: | ||||||||

Cash and cash equivalents | $ | 4,504 | ||||||

Accounts receivable, net | 69 | |||||||

Inventories, net | 5,429 | |||||||

Other prepaid and current assets | 52 | |||||||

Prepaid storage, net of current portion | 659 | |||||||

Developed product intangible | 77,097 | |||||||

Total assets acquired | 87,810 | |||||||

Liabilities assumed: | ||||||||

Other accrued liabilities | 3,327 | |||||||

Other long-term liabilities | 1,094 | |||||||

Total liabilities assumed | 4,421 | |||||||

Total cost of acquisition | $ | 83,389 | ||||||

The fair value of the developed product intangible acquired in the Acquisition was recognized on the basis of relative fair value in accordance with ASC 805, which was estimated utilizing an income approach. The significant assumptions in the estimated fair value of the developed product include the Company’s projected cash flows, the expected life of the product, and a discount rate of 19.5%.

As Enbumyst is a completed product, the developed product intangible asset has been capitalized and will be amortized over its estimated useful life of 10 years. The allocation of the total acquisition cost assumes the Acquisition took place on December 31, 2025. The preliminary cost of the asset acquisition is subject to change as the Company finalizes its valuation of the assets acquired and liabilities assumed, and such changes could be material.

B.Represents the elimination of Corstasis, Inc's historical equity balances, including common stock and accumulated deficit.

C.Represents the net proceeds from the First Amendment Term Loan obtained on the Closing Date, consisting of $25.0 million of gross proceeds less $0.9 million of original issue discount and issuance costs. The First Amendment Term Loan matures on December 31, 2029 and is classified as a non-current liability as it requires no payment until 2028.

D.Represents the net proceeds received from the Royalty Purchase Agreement, consisting of $50.0 million of gross proceeds less $1.3 million of capitalized issuance costs, and the related royalty sale liability. The capitalized issuance costs will be amortized to interest expense over the estimated term of nine years. The Company recorded $4.6 million of the royalty sale liability as current, which reflects the amount the Company expects to repay over the next 12 months.

The following adjustments are reflected in the unaudited pro forma condensed combined statement of operations for the year ended December 31, 2025:

AA. Reflects 12 months of estimated amortization expense related to the acquired developed product intangible asset based on its estimated useful life of 10 years. The amortization expense related to the developed product intangible asset is recorded to Selling, general and administrative.

BB. Reflects 12 months of estimated interest expense recognized in connection with the First Amendment Term Loan described in adjustment C, including amortization of the related issuance costs. The estimated interest expense is based on the effective interest rate as of the Acquisition Closing Date of approximately 10.5%.

CC. Reflects the elimination of the income tax provision recorded in Corstasis's historical statement of operations for the year ended December 31, 2025. As the combined entity maintains a full valuation allowance against its net deferred tax assets throughout the pro forma period, no net income tax expense would have been recognized on a combined basis had the Acquisition occurred on January 1, 2025.

DD. Reflects 12 months of estimated interest in connection with the Royalty Purchase Agreement described in adjustment D. Interest is incurred over the expected term of the Royalty Purchase Agreement using the effective interest method based on the projected payment schedule, which is based on the expected timing of royalties earned under the Company’s Otsuka contract, and an imputed yield of 1.3% per annum, determined at inception.

EE. Represents the pro forma net loss per share for the year ended December 31, 2025. Pro forma basic and diluted net loss per share is computed by dividing the pro forma net loss by the weighted average number of the Company’s common stock outstanding for the year ended December 31, 2025.